Nebius Group: Valuation Model

Nebius Group (NASDAQ: NBIS) has exploded onto the scene of AI infrastructure, rapidly becoming a favourite of retail investors captivated by its staggering growth prospects and the promise of being the new AWS of the AI era. The company’s narrative is built on bedrock: securing multi-billion-dollar deals with Microsoft (up to $19.4 billion) and Meta Platforms ($3 billion), contracts that validate Nebius as a critical sold-out provider of high-performance GPU capacity, and on foundational excellence provided by their engineering team.

Yet, after an astronomical run-up in 2025, the stock has endured a sell-off, plummeting over 30% from its October highs. While this correction reflects investor jitters over AI bubble concerns, a cooling of the AI sector as a whole, and over the interest rate decision - it has simultaneously opened up a massive valuation gap. With analysts still maintaining an average price target of $ 160 (over 60% higher than current levels), this sharp plunge forces a critical question: has the market offered a massive buying opportunity in a high-growth company whose essential infrastructure is perpetually sold out, positioning it to become a winner of the AI revolution?

This article is not a full investment thesis on Nebius. Rather, this is an analysis of how their income statements could look like for the next 3 years, and then an attempt at doing a valuation of the company.

Before diving into the analysis, I’d like to disclose that I am bullish on the company and currently hold a long position. All content provided here is for informational and entertainment purposes only and should not be construed as financial advice. Readers should conduct their own thorough research before making any investment decisions.

Key Bullish Catalysts

While this is not an investment thesis, let’s firstly provide a summary of why Nebius is such a compelling story.

Long term Hyperscaler contracts: Microsoft, Meta.

Offer revenue visibility and act strong validation for Nebius in the short-term

Deals with hyperscalers tend to be more lucrative, helping to fund further capacity expansion

Strategic Shift to Full-Stack AI Infrastructure:

Nebius is moving beyond being a pure raw compute provider to offering a full-stack AI cloud platform, hence the label as the ‘next AWS’.

High-margin software layer (AI tools, developer services) layered on top of the physical infrastructure, which is crucial for driving significantly better overall margins over time compared to simple hardware leasing.

Management reports increasing number of AI savy customers and also report that active customers want to increase use cases by the quarter (hence great customer retention). This is great validation for the SaaS / PaaS layer of the business.

AI specific moat: Specialty Infrastructure vs General Purpose

Building a cloud service for AI specific customers. Nebius specialty and focus on just AI reduces the risk of being taken over by traditional Hyperscalers: GCP, AWS, Azure.

Traditional clouds are general purpose vs Nebius purpose-built AI cloud. This means Nebius can co-exist with the big players, and even become one themselves.

Deepens their moat against their bare metal competitors.

Yandex experience

Core team have previously founded Yandex. They bring deep tech infrastructure and cloud experience after running data centres for more than a decade.

Founder-led companies also align over long term goals and maintain a distinct culture. This, on top of their experience and expertise, is going to differentiate them in this space.

The Subsidiaries: Avride, TripleTen, plus equity in Clickouse and Toloka

Diversified, high-growth and potential businesses on their own

Nebius can leverage the equity in the subsidiaries to fund the Capex growth for its core AI business, rather then going into debt or doing dilution. Competitors like CoreWeave or Iren don’t have this flexibility.

Profit margins: key focus for management

Management has implied that margins are a key driver for their decision making. This is great to hear, because because bare metal IaaS has the risk of being a low a margin business.

SaaS / PaaS layer could improve margins (see AI Cloud point above).

Targeting Inference

Nebius Token Factory. Strategically targeting the massive, untapped market for AI inference. This market is expected to grow faster and scale larger than the training market.

Having said that, now we can move to the forecast models.

Revenue

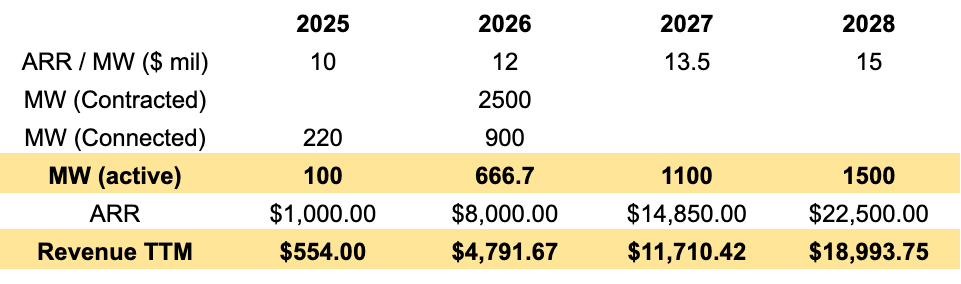

Based on our forecast, Nebius revenue in 2028 would be $19B at 1.5 GW active capacity. While this may seem extremely bullish, the Microsoft deal alone would be carrying ~$3.8B that year on 300 MW (1/5 of the capacity). The forecast matches Citizens and Water Tower’s revenue estimates for 2026-2027, but exceed Goldman’s.

To reach the numbers above, the following assumptions have been made:

Nebius would continue expanding capacity even after activating the guided connected power of 900 MW (sometime in 2027), advancing the roadmap to the 2.5 GW contracted power (albeit in a decelerated manner and not reached during this forecast).

ARR / active MW to expand from current levels (now at ~ $10-12 mil.) due to:

Pricing power on GPU-as-a-service with demand exceeding supply. I am assuming it doesn’t get commoditised in the short or medium term (but still a risk for long term).

Continue landing deals with the Hyperscalers. These deals are more lucrative in the short term, because the Hyperscalers want to get their hands on as much capacity as possible until they finish building their own, hence are willing to pay premium for ready IaaS.

Assuming the SaaS and Inference platform layers start contributing more to the revenue from 2027 onwards. Growth acceleration in customers adopting the full service of the AI Cloud: new customers + existing customers increasing their use cases, as management has said.

Important to note: Hyperscalers will likely not use the full extent of the AI Cloud services, due to them having their own software solutions. Hyperscalers will only be after the bare metal aspect. Hence, the SaaS acceleration would need to come from the other types of customers.

Calculated TTM Revenue by applying a linear monthly growth rate to get from implied Dec-25 revenue ($83.3 mil. from 2025 ARR) → Dec-26 revenue ($666.6 mil. from 2026 ARR), with the same logic applied until Dec-28 revenue. In reality, the monthly revenue growth won’t be as linear and consistent; and it will greatly depend on the timing of contracts and deployment of new capacity - which is something difficult to forecast.

Continuing the trend of selling out capacity as soon as it becomes available.

Assuming revenue from owned subsidiaries is negligible compared to core business, hence not considered in this model.

Based on today’s market cap of approx. $25B at $100 / share, Nebius would be trading at 5.25 Fwd P/Sales 2026.

Capex

Industry experts estimate ~ $38B of Capex required to get to 1 GW of active capacity. Hence, the rate of $38 mil / MW was the assumption used to forecast the required Capex. Given the assumed MW roadmap from the previous section, the yearly breakdown would be:

2025: $5B - already guided

2026: $15.57B

2027: $18.43B

2028: $15.2B

Post-2025, cumulative Capex would need to be $49.2B. This breeds the question, how will Nebius be able to afford this?

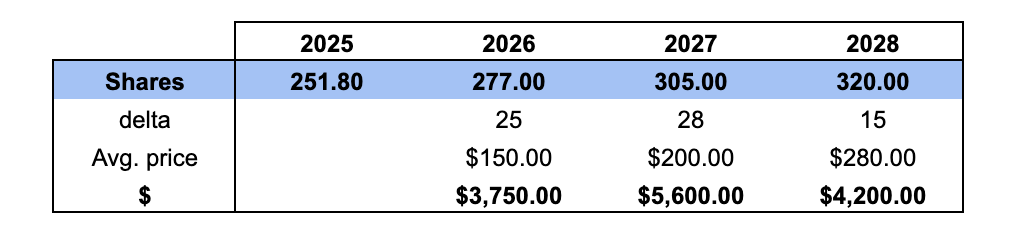

Management has mentioned they will utilise at least 3 sources of financing to support the Capex: corporate debt, asset-backed financing and equity. On the equity front, they have announced a program of up to 25 mil. shares in dilution. They also mentioned they will remain dilution sensitive to continue financing future growth. Hence, we should expect even more dilution programs to follow:

The dilution would raise about $13.5B over the years. In addition, according to my income statement model (see later section in detail), Nebius would bring about $22.8B in EBITDA through 2026-2028, which I am assuming would go straight into Capex. This would leave Nebius short of the required Capex by ~$13B. This could be covered by the other 2 methods:

Debt

Management believe this will be on attractive terms, as it’s supported by the creditworthiness of their largest customers: MSFT, META.

As of Q3 25

Total Debt of $4.5B

Positive Equity of $4.8B (Total Assets - Liabilities)

Nebius maintains good working capital and are not financially strained in the short-term: Current Assets $5.2B vs Current Liabilities $790m.

I am assuming that by the time they raise the required $13B of debt, Nebius would have even more than that in assets, so they wouldn’t be in a net negative position.

Selling equity from the non-core business units

I believe they will wait longer to use this option, in order to give the subsidiaries more time to mature and increase their value. Timing of potential Clickhouse and Avride IPOs would be key.

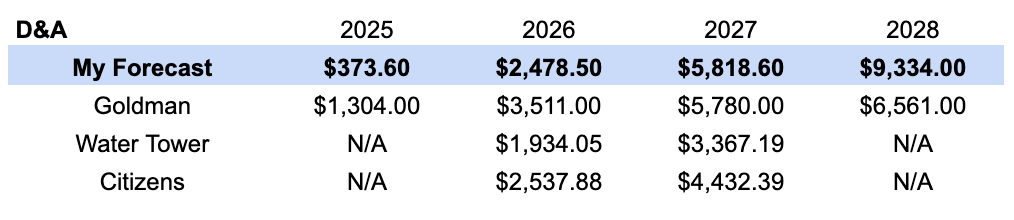

Depreciation

As for the depreciation, assumed the yearly Capex numbers from the previous section to be evenly split by quarter, and then applied the specific D&A cycle to each asset class as following:

Compute (GPUs/Servers) - approx 80% of Capex (as Arkady mentioned during Q3 call) was depreciated over 4 years (as preferred by the Nebius team)

Infrastructure (Shell, Power, Cooling) - rest of 20% depreciated over 15 years (a conservative blend between 10-12 yr for cooling/power sys. and 20-30 yr for the building).

This would lead to $17.6B in cumulative D&A between 2026-2028. The table below shows the yearly breakdown (quarterly breakdown to be shown in the Income Statement section), compared also to what analysts have forecasted. While my D&A may seem more pessimistic, it’s possible the analysts assumed Nebius would stop at the 900 MW mark , rather than keep investing → estimated less Capex (+ also less revenue).

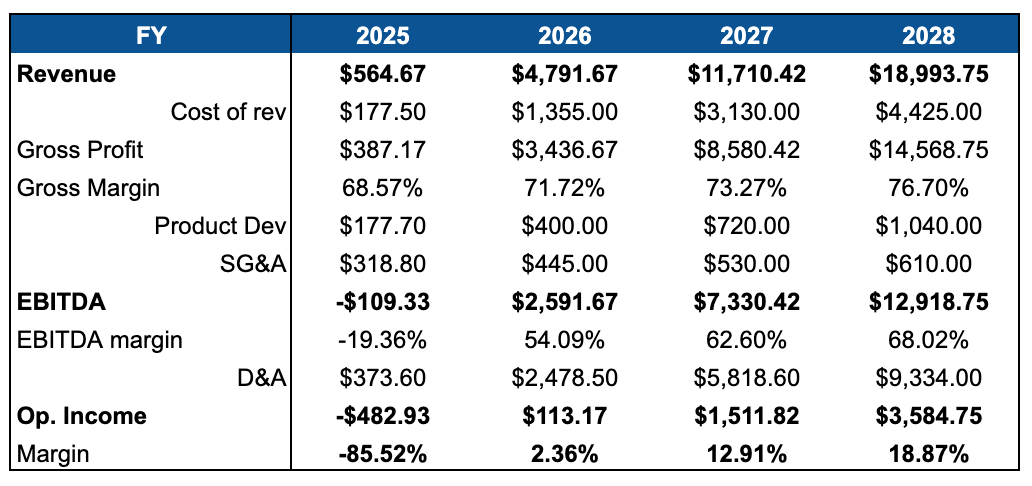

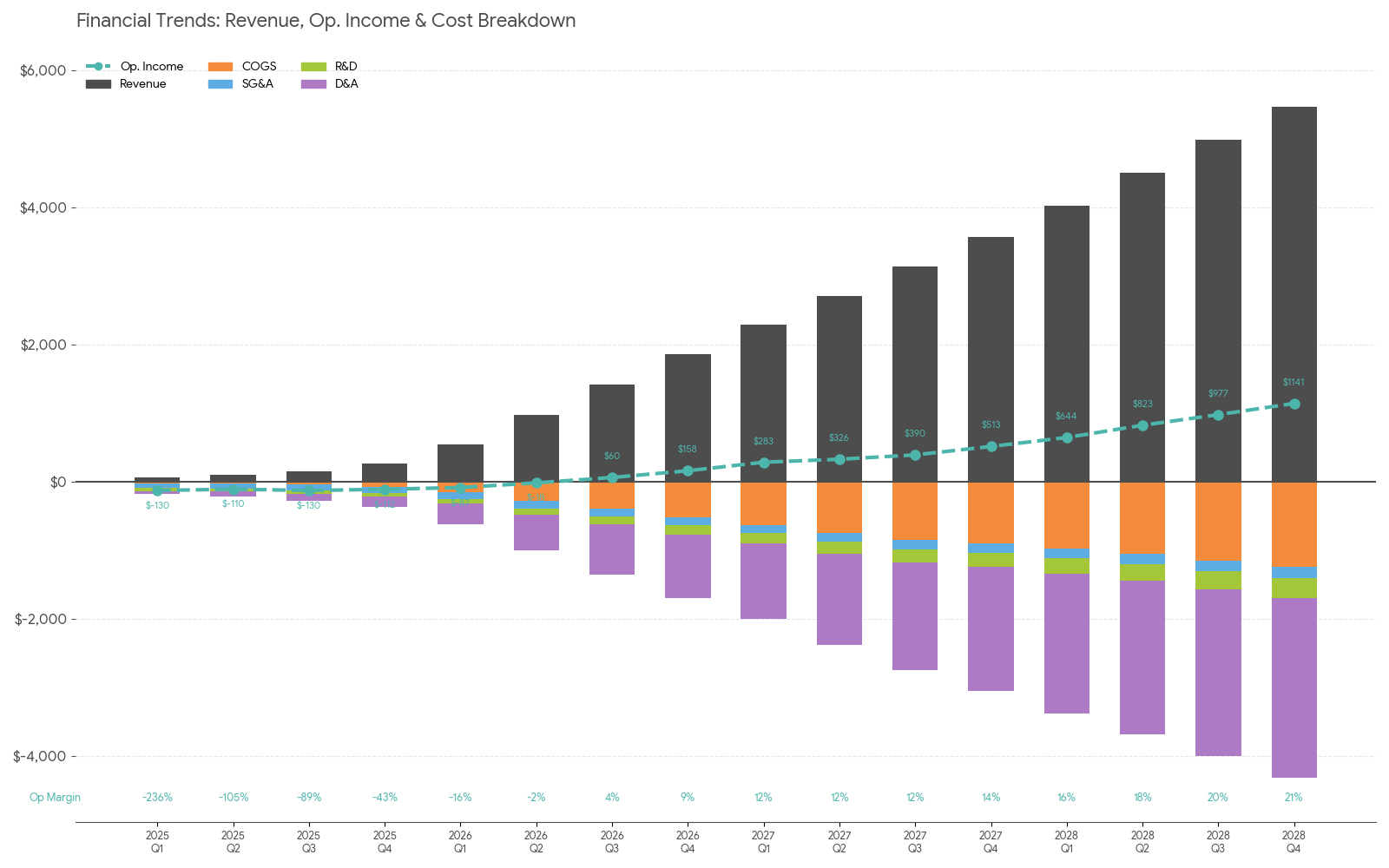

Income Statement

For the income statement projection:

Incrementally increased Gross margins to illustrate the pricing power related to capacity being a hot commodity, extra contributions from the growing SaaS layer and to account for natural efficiency increase at scale. Goldman Sachs also had gross margins expanding to 75% and 77% in 2027 and 2028.

Grew Product Dev expense by about $300 mil. a year (CAGR of 80%) and SG&A by about $90 mil. a year (CAGR of 24%). Assuming R&D into new verticals and expanding the software side is going to be a big part of the growth roadmap post capacity expansion phase.

EBITDA margins match the consensus among analysts (Goldman, Citizens, Water Tower).

Operating margins are the ones getting hit by the aggressive D&A, but still projected to get to 19% for year 2028 and peak by quarter at ~21% in Q4 2028.

Decided not to include Net Income due to having no visibility over the interest expenses. Instead, will use EBIT margins (Op. margins) for valuation, because management has offered mid-term guidance of 20-30%.

The model ended up not achieving Management’s mid-term guidance of 25% EBIT margins within the analysed time-span. However, judging by the trend, it is certainly possible the 25% target would’ve been hit in the next 1-2 years. It is up to everyone’s interpretation of what time-span constitutes the ‘mid-term’. Even so, with the heavy D&A expenses but also with a lofty Revenue prediction, Nebius would be able to hit 20% EBIT margins, which is the lower end of their guidance.

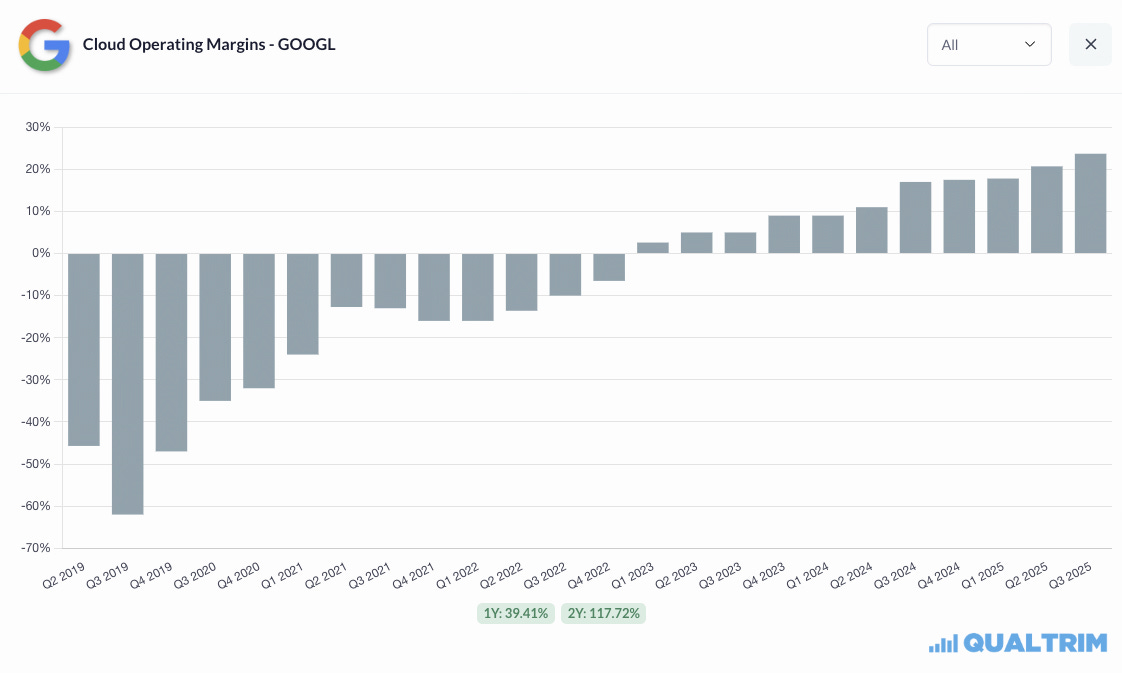

While not a perfect comparison due to having different business models, Google only just recently hit 20% operating margins on their cloud business, and reached positive margins 3 years ago. So management’s guidance is very ambitious.

Valuation

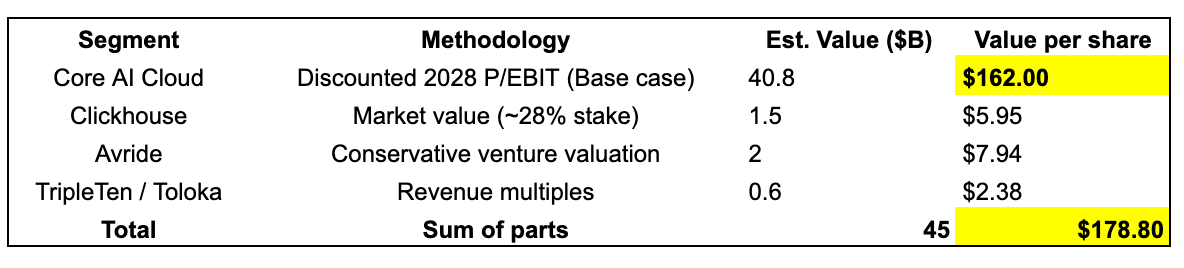

Core Business

Projected EBIT is the selected metric to value the core business, which based on the model would be $3.6B in 2028.

Given the triple-digit growth profile and “sold-out” capacity dynamics, a 20x - 30x P/EBIT multiple on 2028 numbers is justifiable.

As mentioned before, we also assume the share count expands to ~320 million shares by 2028.

Bear Case (20x EBIT): $224 ($71.7B market cap) EOY 2028

Base Case (25x EBIT): $280 ($89B market cap) EOY 2028

Bull Case (30x EBIT): $336 ($107.5B market cap) EOY 2028

Discount to Present: applying a very conservative 20% discount rate (accounting for execution risk) yields the following present values:

Bear Case: $130 EOY 2025

Base Case: $162 EOY 2025

Bull Case: $194 EOY 2025

Note: The base case aligns closely with the current analyst consensus target of $160, suggesting the market is efficiently pricing in the execution of the 1.5GW roadmap.

Subsidiaries

The market currently seems to be assigning zero or negative value to Nebius’s subsidiaries, which is where the asymmetric upside lies. These assets are not mere distractions; they are late-stage, venture-backed businesses.

ClickHouse (Database): Nebius holds a ~28% stake. This is one where an IPO in the mid-term is very likely, potentially at about $15-25B. With ClickHouse’s current valuation estimated at over $5 billion in recent secondary markets, this stake alone is worth ~$1.4B - $1.5B.

Avride (Autonomous Driving): Recently secured $375M in financing backed by Uber. Analysts at DA Davidson have suggested Avride alone could be worth between $5B and $10B in the future. A future IPO could push Avride’s value to $20B, but dilute Nebius to a ~30% stake. Conservatively valuing Nebius’s stake at $2.0B today provides a significant margin of safety.

TripleTen (EdTech): With bookings run-rates exceeding $60M and profitable unit economics, a 2x sales multiple values this asset at ~$120M.

Toloka (Data Labeling): Following the pivot to GenAI data and the investment from Bezos Expeditions, the Nebius stake is estimated at ~$500M.

Sum-of-Parts (SOTP) Summary

Conclusion

Finally, it would be appropriate to acknowledge that Nebius is a very challenging company to value, participating in an environment which carries a lot of risks … but also a lot of upside as well. They are undertaking a historic build-out (along with other players too).

The sell-off presents a classic market dislocation. Investors are currently pricing the stock solely on the immediate risks of the core infrastructure build-out (dilution, Capex intensity, jitters around AI market as a whole) while ignoring the immense earnings power of the 2027-2028 roadmap and arguably assigning zero value to a portfolio of unicorns (Avride, ClickHouse) embedded within the holding company.

Even with a lot of assumptions being quite conservative, our model suggests that if Nebius simply executes on its stated roadmap to 1.5 GW of capacity, the core business alone supports a share price of $160+ today. When layering in the conservative value of the subsidiaries, the fair value pushes toward $170-$180, offering a discrepancy of 60-70% from current levels.

Nebius is not just a hardware rental company; it is a full-stack AI cloud provider with the DNA of a tech giant. For investors willing to stomach the volatility of the AI trade, NBIS represents one of the few remaining “ground floor” opportunities to own a potential Hyperscaler.

If you enjoyed this article, please remember to give us a follow on X (@DeepdiveEcon).

We try to see through the noise and provide numbers-based analysis. Many people guess … let’s understand!

👏🏽

here’s mine: https://open.substack.com/pub/investorinmisunderstoodcos/p/nebius-update-valuation-model?r=4b7zut&utm_medium=ios&shareImageVariant=overlay